1 in 5 Small Businesses Owe Money to the IRS, and What This Means for Commercial Lenders Published March 14, 2021

The IRS Wait is Over: Back to Reality

As a result of the pandemic, the IRS intermittently opened and closed throughout 2020, impacting their ability to maintain operations. They struggled to deal with basic business operations, such as opening the mail and picking up the phone — much less able to process paperwork or go after businesses and individuals for their tax debts.

The Peoples First Initiative went into place on March 25, 2020, to help alleviate taxpayers’ financial burden. This initiative was scheduled to expire in July but was extended through August, then September, and finally was lifted in October of 2020. This means that as of October of last year, the IRS collection engine has restarted. Businesses that were able to get some temporary relief from making fewer tax deposits, if any at all, are now having to face the reality of their increasing tax debts.

As of October 1, 2020, the IRS instructed staff to resume normal operations in their collection activities – assessing new tax debts, filing federal tax liens, issuing levies (seizure of assets), and defaulting payment agreements when scheduled payments didn’t resume.

What Does This Mean for Commercial Lenders?

While businesses operated under the IRS radar for several months in 2020, this dead period is now over. As the IRS increases operations, including assessing balances due and filing more liens, this means that the outstanding tax debts will wreak additional havoc on businesses’ cash flow–with businesses having little choice in the matter. Many businesses are already struggling with cash flow issues and now, these off-balance sheet liabilities will mean the IRS will resume aggressively collecting money before other debts are paid.

To help evaluate and determine the financial health of a borrower, commercial lenders typically utilize the following common due diligence tools and documents:

- Tax returns

- Search for federal tax liens

- Bank statements

While this information can be useful, it does not provide the full picture. We’ll explain why relying on lagging indicators versus leading indicators can negatively impact lenders.

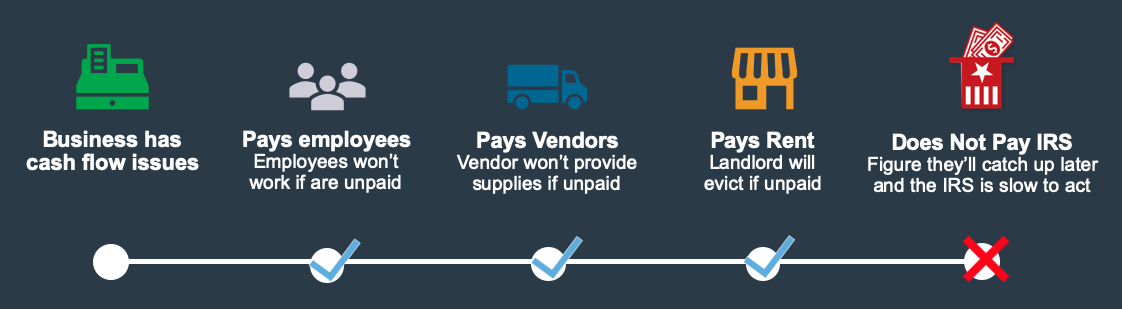

Distressed Businesses Pay the IRS Last

The chart below illustrates the common order of operations for distressed businesses paying their bills in a cash flow crunch. When a business runs into cash flow issues, it becomes a first-things-first order of operations for making payments.

Obviously, it’s of paramount importance to cover payroll so employees continue to come to work. Next, a business will pay vendors to continue supply flow, and cover rent if necessary to maintain a storefront, office or warehouse space.

This leaves the IRS payroll tax deposits last on the list of priorities because most businesses assume they can catch up later with the IRS when their cash flow situation improves, even if they are accumulating fees and penalties in the meantime. Therefore, insight into a business’ payroll tax deposits compliance is a leading indicator of financial distress in a business.

Once the IRS assesses these debts, it becomes a hidden off-balance sheet debt that does not show up in traditional lending due diligence. However, it can be a key predictor of future credit defaults, even if a lien is never filed, putting the IRS debt in the way of all other business debt.

The Amount of Businesses Who Owe the IRS Money Will Continue to Increase

After recently reviewing historical tax data across all industries and geographies, we discovered that 22% of all businesses owe money to the IRS with no public record of a federal tax lien filed.

We discovered that 22% of

all businesses owe money to

the IRS with no public record

of a federal tax lien filed.

This data is foreshadowing what is to come.

There’s more uncertainty in small business cash flow situations than ever and the current toolkit to assess their health is insufficient. With the IRS revving their pent-up collection engine, businesses will also be running into more trouble with the IRS. It’s just a matter of time before the IRS regime uncovers these debts, which creates compounding cash flow issues for these businesses—with little warning or relief. This can be a devastating blow to businesses, putting them at risk, causing them to default on their loans.

Commercial lenders can avoid these worst-case scenarios by leveraging tax data to gaining deeper insights into their borrowers and portfolios.

Contact us for a customized demo to see how we help lenders uncover credit risks today.